【2026 Gen Z Consumer Behavior Survey Report】Gen Z Cannot Be Lumped Together! Segmenting into Three Generations Reveals Clear Differences in Consumer Behavior! OASIZ “New Structure of Gen Z Decoded Through Three Layers”

OASIZ Inc. (Headquarters: Shibuya-ku, Tokyo; President & CEO: Yu Eto; hereinafter “OASIZ”), a next-generation company specializing in vertical short-form videos such as TikTok, conducted a survey on “Gen Z Consumer Awareness and Social Media Usage” targeting men and women aged 15-29 nationwide. While Gen Z is often discussed as a single entity, our analysis reveals clear differences in consumer behavior and values among three segments: “Z1 (15-19 years old),” “Z2 (20-24 years old),” and “Z3 (25-29 years old).”

We present the reality of the “Three-Layered Z Era” that cannot be grouped together: “Z1” who make instant purchases based on trends, “Z2” who choose based on stories, and “Z3” who compare and purchase with conviction.

■ Survey Background

Gen Z, born between the late 1990s and early 2010s, has gained attention as a “digital native generation” that expresses themselves and gathers information through social media. However, within the 15-29 age range called Gen Z, the environment in which they grew up has changed significantly, resulting in completely different values, and we believe that describing them with the single term “Gen Z” is not optimal from a marketing perspective.

At OASIZ, through our social media marketing efforts targeting Gen Z on platforms like TikTok, we have observed a tendency that “even within Gen Z, responses to trends and purchase motivations are completely different.”

Therefore, we conducted a quantitative survey targeting men and women aged 15-29 nationwide and performed data analysis to “segment and redefine Gen Z.” As a result, it became clear that Gen Z exhibits distinct consumer behavior characteristics in each generation: “Intuitive Z1,” “Empathetic Z2,” and “Rational Z3.”

■Survey Summary

This survey was conducted targeting people aged 15-29 living throughout Japan. We divided them into three age-based segments: “Z1 = 15-19 years old,” “Z2 = 20-24 years old,” and “Z3 = 25-29 years old,” analyzed the consumer behavior and values of each generation, and reveal the reality of Gen Z that “can no longer be grouped together.”

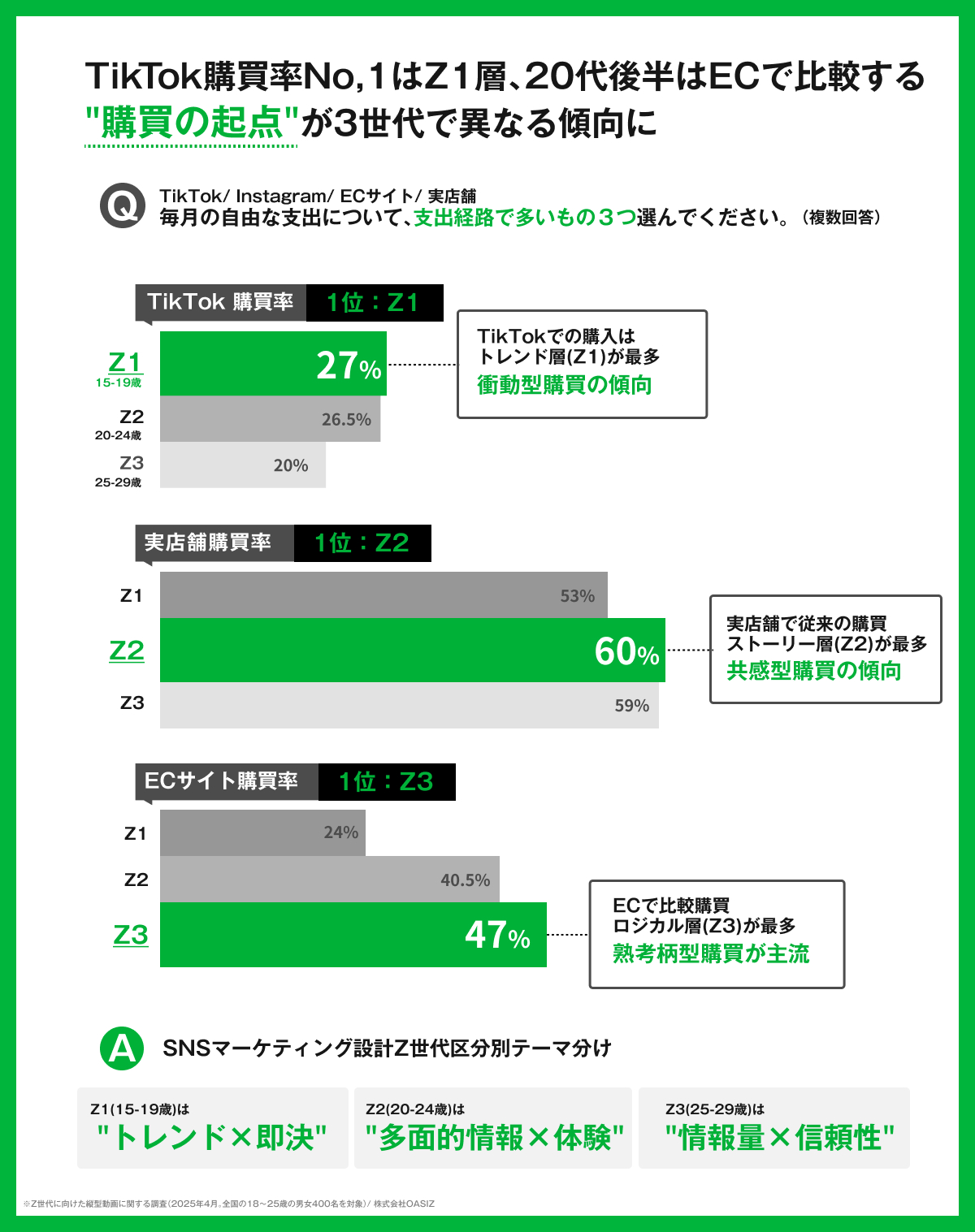

Z1 Buys on TikTok, Z3 Compares on EC. “Purchase Starting Points” Divided by Generation

When we surveyed the main purchasing channels for monthly discretionary spending, it became clear that the starting points for purchases differ significantly even within Gen Z depending on age group. Purchases via TikTok are highest among Z1 (15-19 years old) at 27%, with the percentage declining as age increases through Z2 (20-24 years old) and Z3 (25-29 years old). Meanwhile, in-store purchases are highest among Z2 at 60%, exceeding both Z1 and Z3. Furthermore, EC site purchases are highest among Z3 at 47%, showing a large gap with Z1 (24%).

These results suggest that Z1 has a strong tendency to move from trending content on social media to impulsive and intuitive purchases, while Z2 values in-store experiences and empathy, and Z3 makes purchases after comparing and evaluating information on EC sites.

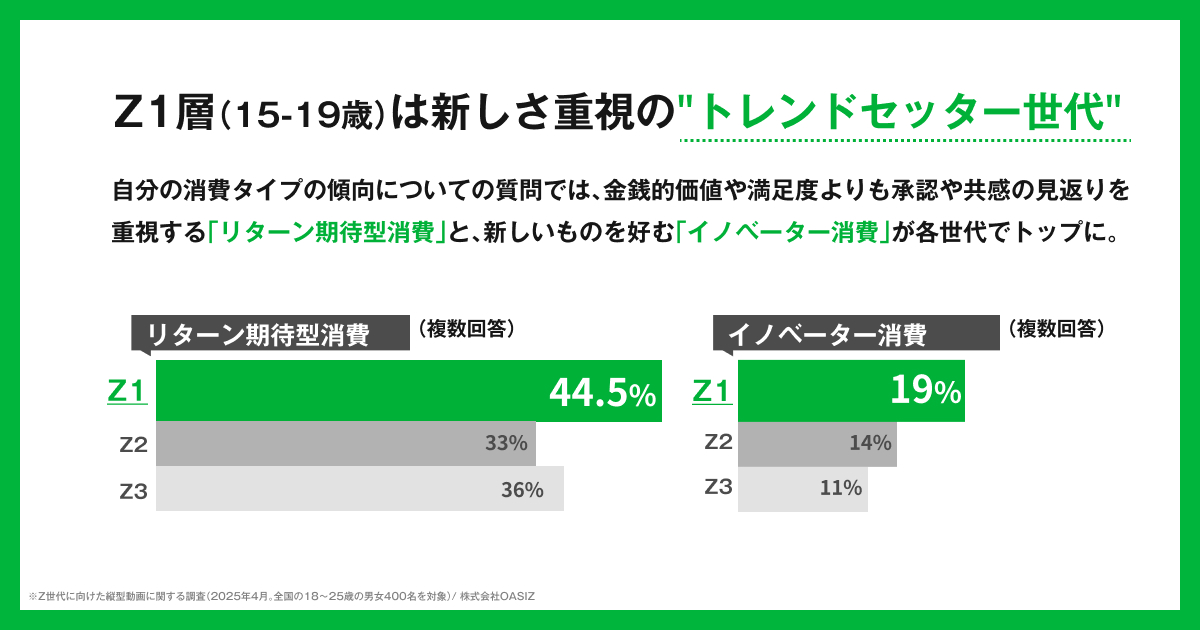

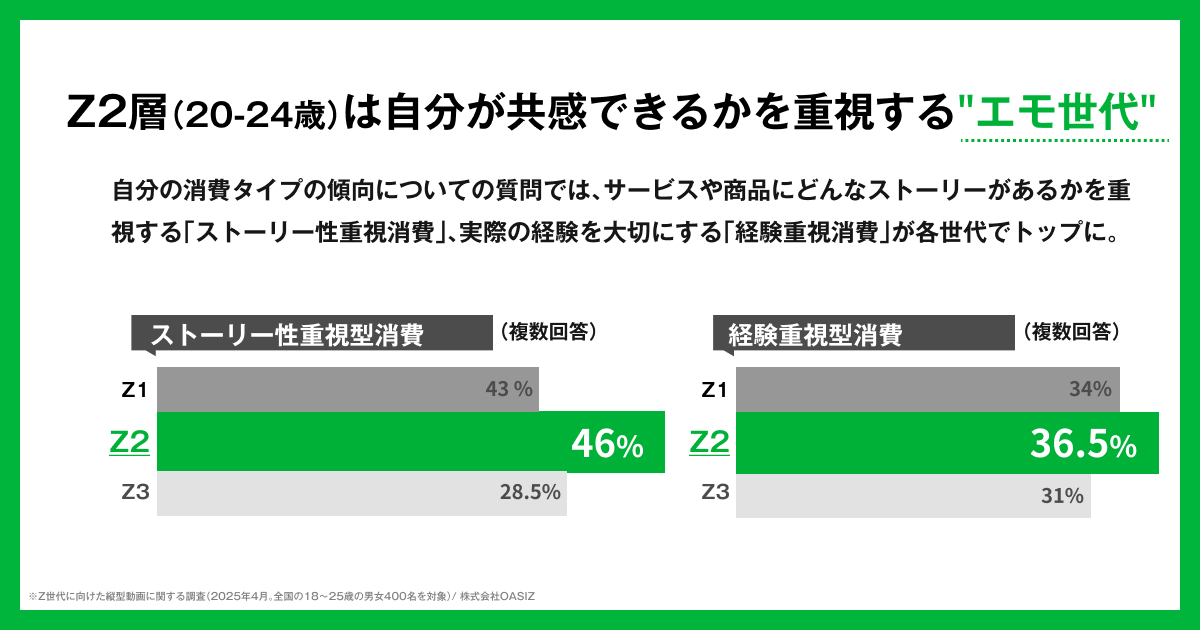

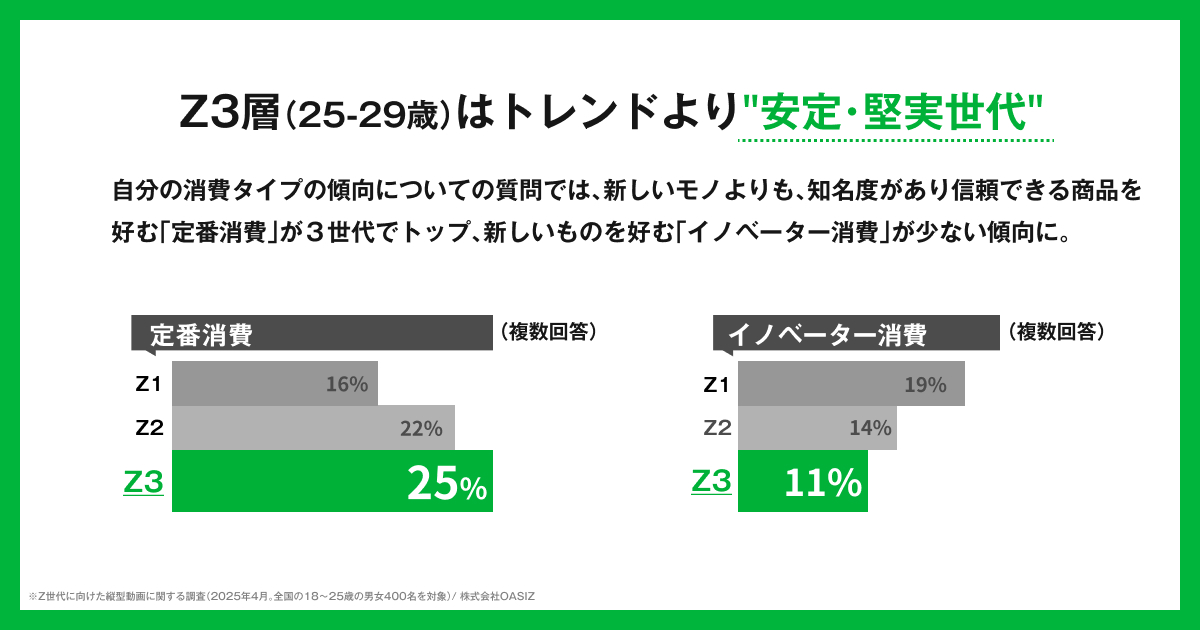

Three Different Consumer Behaviors Revealed! Z1 is the “Trendsetter Generation” Prioritizing Novelty, Z2 is the “Emotional Generation” Valuing Product Stories, Z3 is the “Stable and Prudent Generation” Choosing “Reliable Satisfaction” Over Trends.

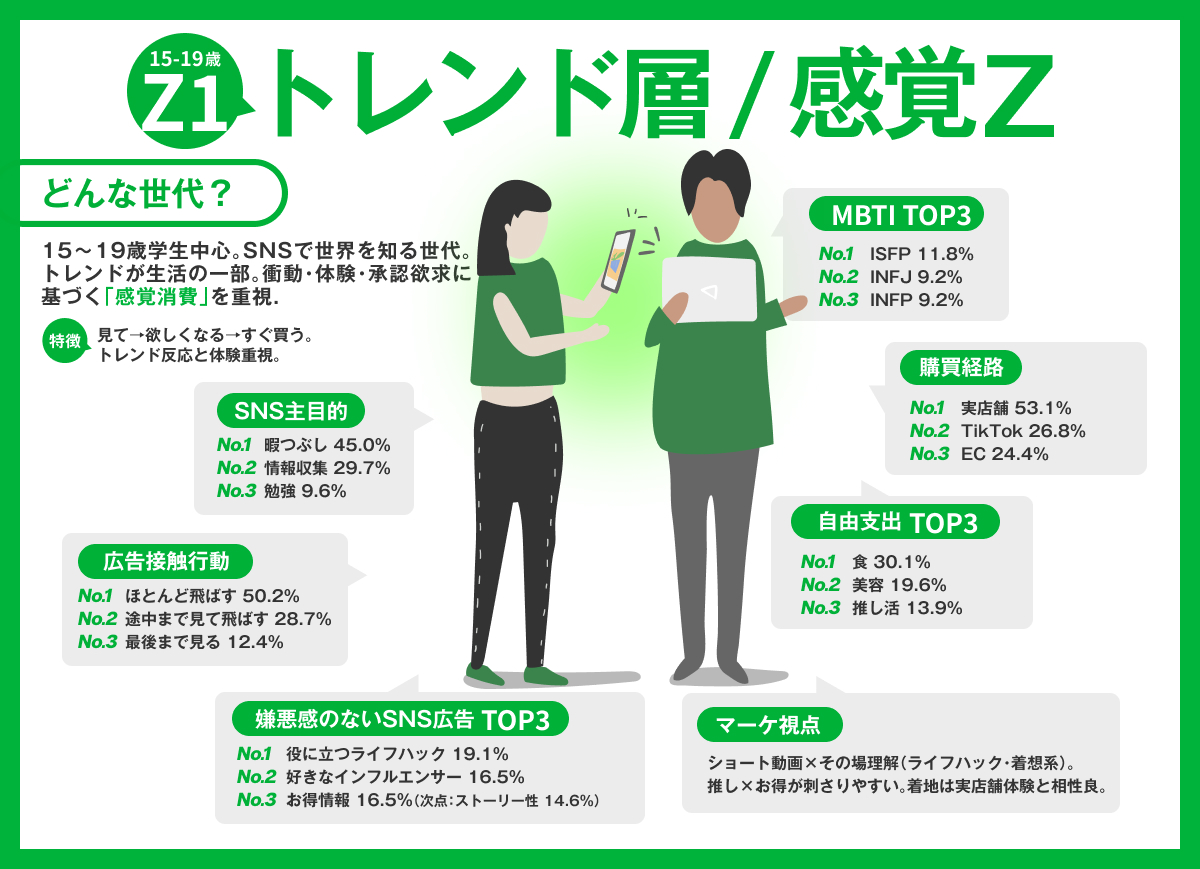

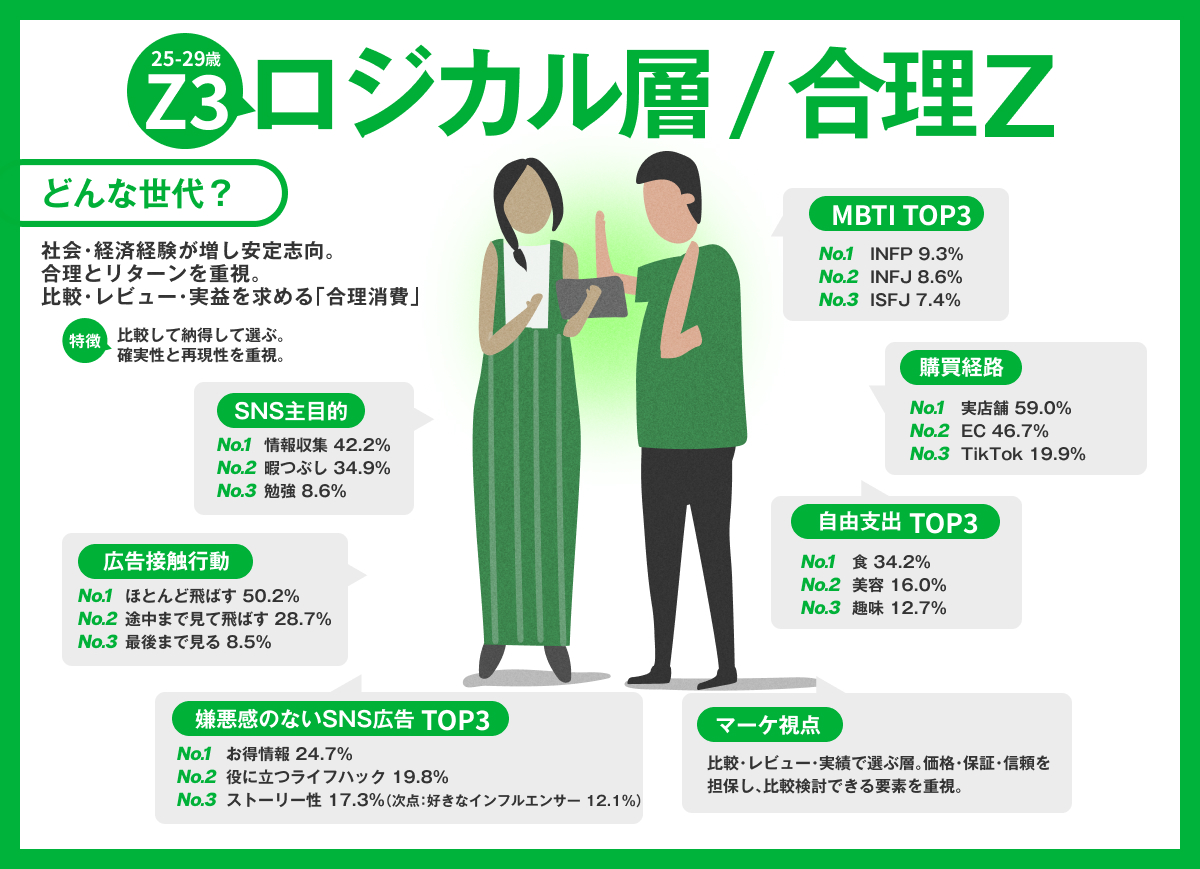

When comparing consumption type tendencies by generation, it became clear that value judgment criteria differ markedly even within Gen Z. Z1 (15-19 years old) shows high percentages of “Return-Expecting Consumption,” which values obtaining “responses” such as approval and empathy through purchases, and “Innovator Consumption,” which actively embraces new and trending items, with consumer behavior characterized by trend-driven purchases. Meanwhile, Z2 (20-24 years old) has the highest percentages for “Story-Focused Consumption,” which values the background and thoughts behind products and services, and “Experience-Focused Consumption,” which values actual experiential value, suggesting that whether they can empathize becomes the axis of purchase decisions. In contrast, Z3 (25-29 years old) shows the highest percentage among all three generations for “Standard Consumption,” which prefers well-known, proven, and reliable choices, with a prudent consumption style that emphasizes trustworthiness and stability over novelty. These results suggest that for Gen Z-targeted initiatives, generation-specific communication design is effective, focusing on novelty and virality for Z1, empathy and experience for Z2, and trustworthiness and information depth for Z3.

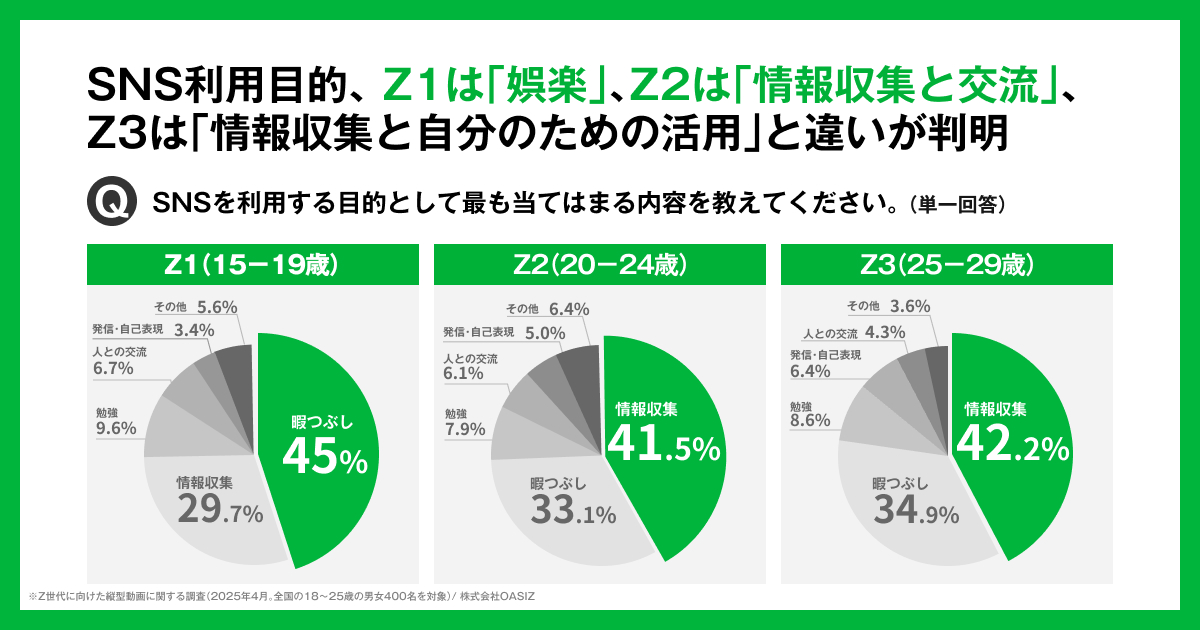

SNS Usage Purposes Differ: Z1 for “Entertainment,” Z2 for “Information Gathering and Interaction,” Z3 for “Information Gathering and Personal Use”

Analysis of the “primary purpose (most applicable)” of SNS usage by age revealed that the positioning of social media differs significantly even within Gen Z. Among Z1, “killing time” was most common at 45.0%, showing a prominent tendency to use SNS as a place for entertainment.

Meanwhile, among Z2, “information gathering” was highest at 41.5%, showing a tendency toward higher emphasis on practical information acquisition while using it for entertainment in parallel.

Furthermore, among Z3, “information gathering” was highest at 42.2%, showing a similar tendency to Z2, but “posting/self-expression” was next most common after studying, making it clearer that they use SNS as “a tool to help their own life and decision-making.” These results show that SNS is not a uniform entertainment medium for Gen Z, but rather its role changes with age from “entertainment → information acquisition → practical utilization.”

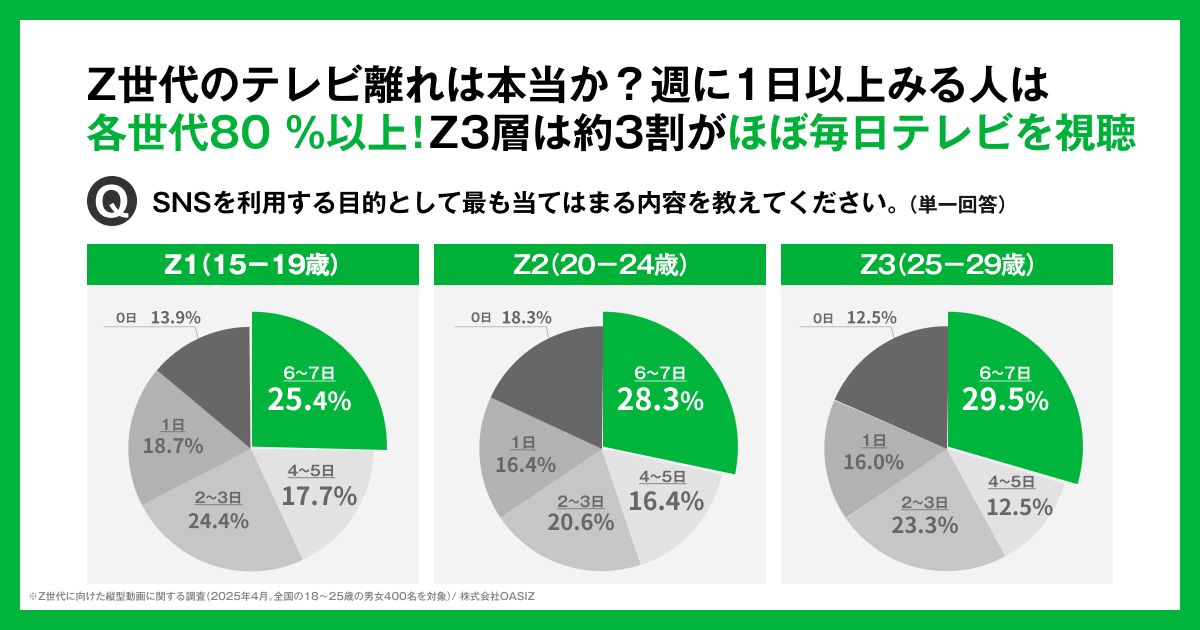

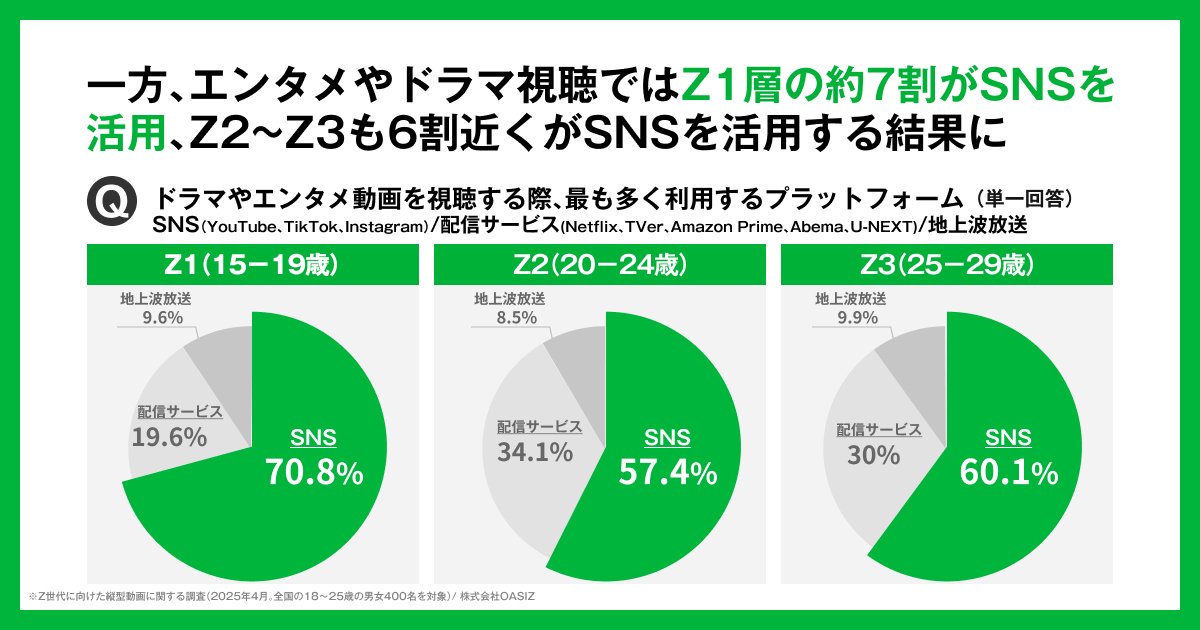

Gen Z Is Not Abandoning Television! “Role Differentiation” Revealed: SNS for Entertainment Viewing, Television for Daily Contact

Furthermore, it became clear that “television離れ (TV abandonment)” is not uniformly progressing among Gen Z. The percentage of people who watched television (excluding streaming services) for one or more days in the past week exceeded 80% in all Z1-Z3 generations, with approximately 30% of Z3 (25-29 years old) watching television “almost daily (6-7 days).” On the other hand, when looking at the main platforms for viewing entertainment and drama content, approximately 70% of Z1 and around 60% of Z2 and Z3 use SNS (YouTube, TikTok, Instagram) most frequently. These two results suggest that while Gen Z has daily contact with television as a device, they tend to consume entertainment and drama content that they actively enjoy starting from SNS. Television viewing is centered on daily life-flow contact such as “seeing” or “hearing” news programs and information programs while having them on, and the main battleground for entertainment content has likely shifted to SNS.

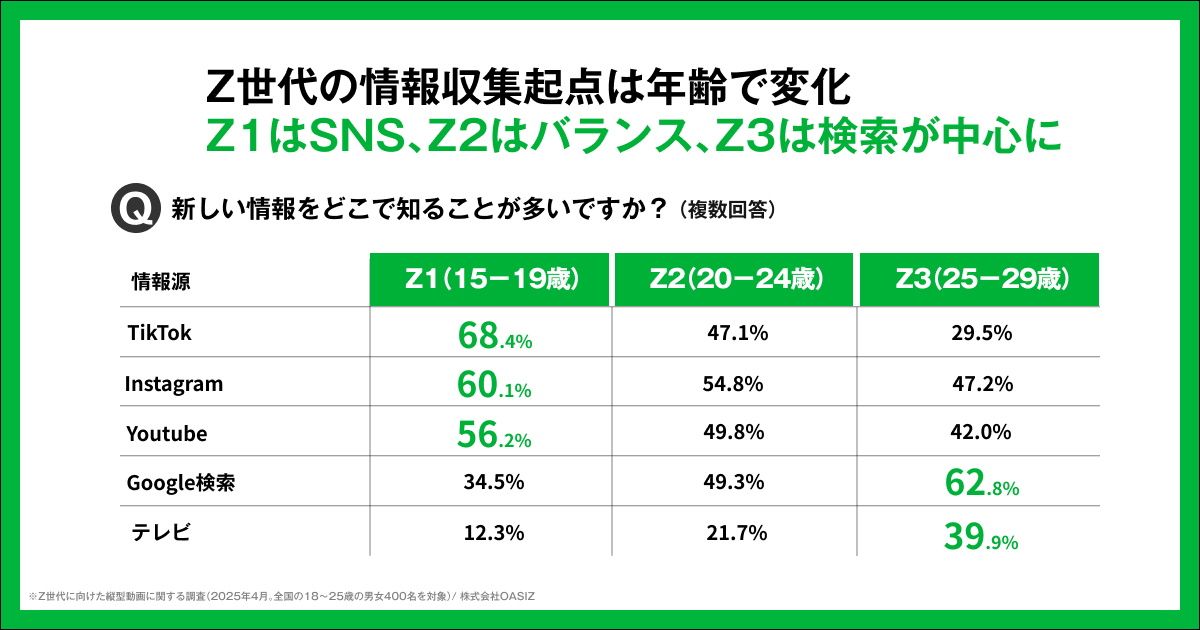

Gen Z Information Gathering Starting Points Change with Age! Z1 Centers on SNS, Z2 is Dispersed, Z3 Centers on Search

When looking at the starting points for obtaining new information by generation, clear differences were observed even within Gen Z. For Z1 (15-19 years old), SNS platforms such as TikTok (68.4%), Instagram (60.1%), and YouTube (56.2%) are the center of information gathering, with serendipitous information contact through short-form videos being mainstream. Meanwhile, for Z2 (20-24 years old), in addition to SNS, Google search (49.3%) usage is also high, showing a tendency to gather information while using multiple sources. In contrast, Z3 (25-29 years old) shows the highest usage of Google search (62.8%), with television (39.9%) usage also higher compared to other segments, revealing that they emphasize active information gathering that values reliability and comprehensiveness.

These results suggest that within Gen Z, as age increases, the role shifts from SNS-based to information gathering utilizing search engines and mass media.

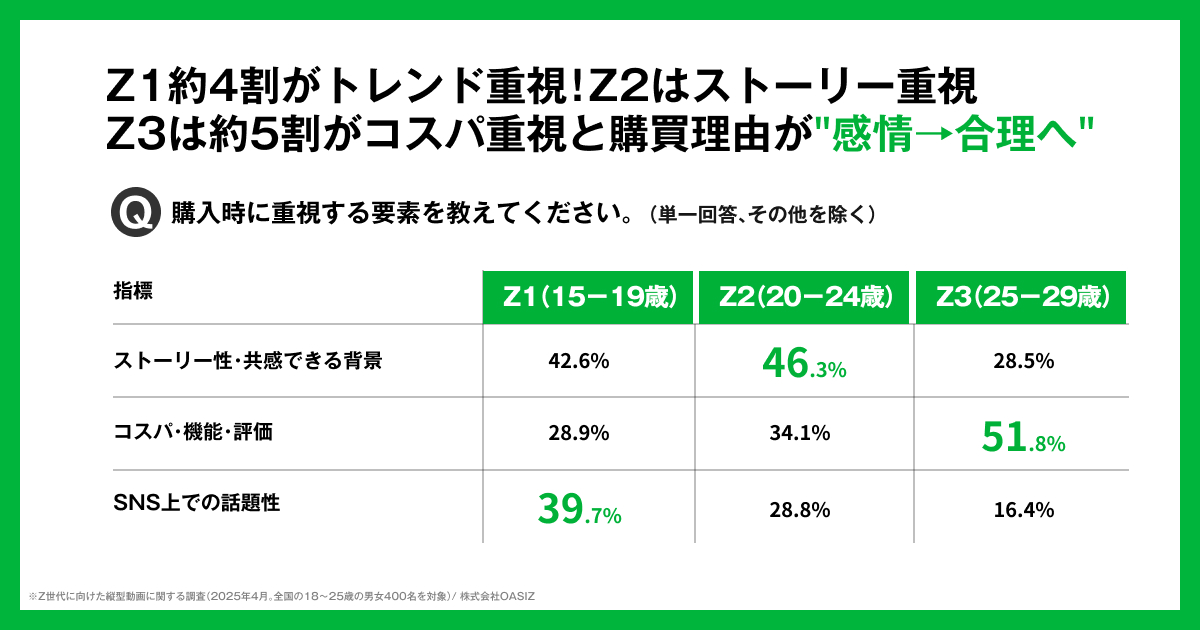

Approximately 40% of Z1 Emphasize Trends! Z2 Focuses on Stories, Approximately 50% of Z3 Emphasize Cost-Performance, Purchase Reasons Shift from Emotional to Rational

When looking at factors emphasized during purchase by generation, it became clear that judgment criteria change progressively within Gen Z.

For Z1 (15-19 years old), “buzz on SNS” is high at 39.7%, with whether something is trending being a major purchase driver.

Meanwhile, Z2 (20-24 years old) shows “story/empathetic background” as most common at 46.3%, suggesting that empathy with the thoughts and context embedded in products and services influences purchase decisions.

In contrast, Z3 (25-29 years old) shows “cost-performance, functionality, reviews” accounting for 51.8%, nearly half, with a prominent tendency to emphasize rational indicators such as price, functionality, and reviews. These results suggest that Gen Z purchase reasons shift with age from trend- and emotion-based judgments to more rational judgments.

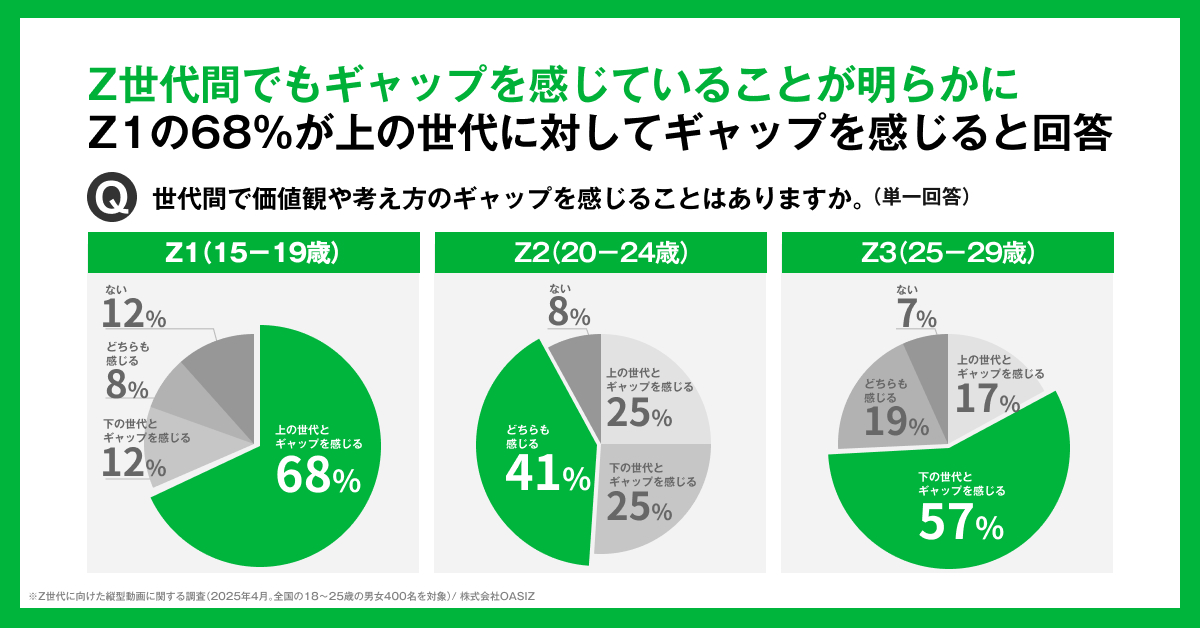

Gaps Felt Even Among Gen Z Revealed! 68% of Z1 Feel Gaps with Older Generations

When surveyed about whether they feel gaps in values and ways of thinking between generations, it became clear that even within Gen Z, perceptions differ by age. Among Z1 (15-19 years old), 68% responded that they “feel a gap with older generations,” a prominently high result showing strong awareness of differences in values and behavioral patterns. Meanwhile, the percentage feeling “a gap with younger generations” remained at only 12%.

In contrast, among Z2 (20-24 years old), “feel both” was most common at 41%, showing a “middle generation” position where they feel value differences with both older and younger generations. Furthermore, among Z3 (25-29 years old), “feel a gap with younger generations” was highest at 57%, showing that as age increases, the target of perceived gaps shifts to younger generations. These results reveal that Gen Z is not monolithic, and even within the same generation, they feel gaps based on differences in position and experience.

“Gen Z Cannot Be Grouped Together. Marketing Enters the Era of ‘Three-Layered Z Design'”

Through this survey, it became clear from the research that Gen Z is not an entity that can be grouped together, with significantly different psychological backgrounds and consumer behaviors.

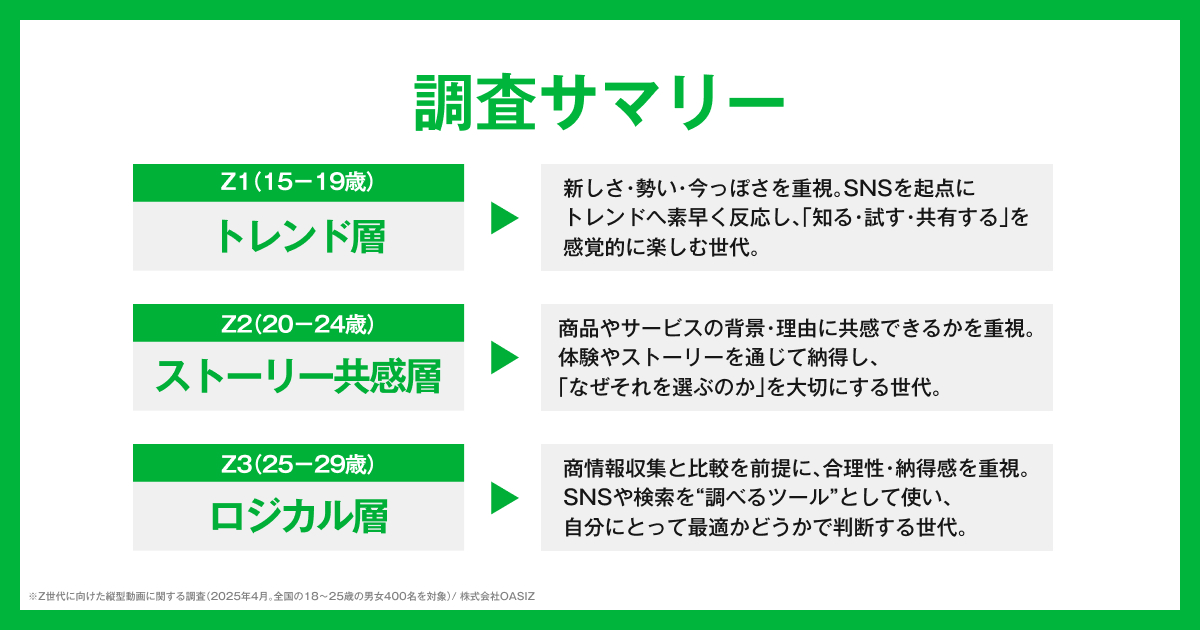

Z1 (15-19 years old) is a “Trend Layer” that acts intuitively based on trends and momentum, Z2 (20-24 years old) is a “Story Empathy Layer” that values empathy with the background and stories of products and services, and Z3 (25-29 years old) is a “Logical Layer” that seeks rationality and conviction based on information gathering and comparison, each making decisions based on different value criteria. Going forward, in marketing and communication targeting Gen Z, we believe it will be important to have a clear “three-layered Z design” that specifies which segment the communication targets, rather than a uniform “for Gen Z” design.

■ Survey Overview

Survey Name: Gen Z Consumer Awareness Survey

Conducting Organization: OASIZ Inc.

Survey Target: Ages 15-29

Gender: Male and Female

Region: Nationwide

Survey Method: Internet Research (Knowns Inc. “knowns”)

Survey Period: September 2025 – October 2025

Valid Responses: n=1,201

<Terms of Use>

Please specify “OASIZ Inc.” as the source of information. *Please refrain from citing or reprinting with modifications to part or all of the survey content.

PRTIMES: https://prtimes.jp/main/html/rd/p/000000035.000100857.html